At the “Forum New Energy World” conference hosted by Conexio in Berlin in September, 2022, one session posed a provocative question: “Three thousand [GW] instead of 300 GW of solar additions – crazy idea or hard-hitting reality?”

Ten years ago, pv magazine and the forum – at that time, both part of renewable energy consultant Solarpraxis AG – suggested a similarly utopian figure by launching a campaign to reach 300 GW of annual global PV additions in 2025. Back in 2012, talk in Germany concerned solar taxes, over-subsidization, and the 52 GW solar capacity ceiling. Nevertheless, Solarpraxis founder Karl-Heinz Remmers called for Germany to hit 200 GW of cumulative PV by 2025, alongside the global 300 GW annual goal.

Since then, the German government has adopted a goal of 215 GW of solar this decade and the world will probably see 300 GW of new solar installations this year. It is now widely accepted that an increased solar ambition is required to address climate change and energy security. With the electrification of heat, transport, and other sectors opening up potentially huge markets for solar, what should the target be?

In my remarks in the forum session I provided the international context and tapped our global network of reporters to shed light on the situation and outlook of key PV markets.

I drew upon trade body SolarPower Europe’s “Global Market Outlook 2022-2026,” and the world’s three biggest solar markets – China, the United States, and India – were assessed by Vincent Shaw, Anne Fischer, and Uma Gupta, respectively. Pilar Sanchez, in Valencia, provided an update on Spain, Europe’s second-biggest PV market, after Germany.

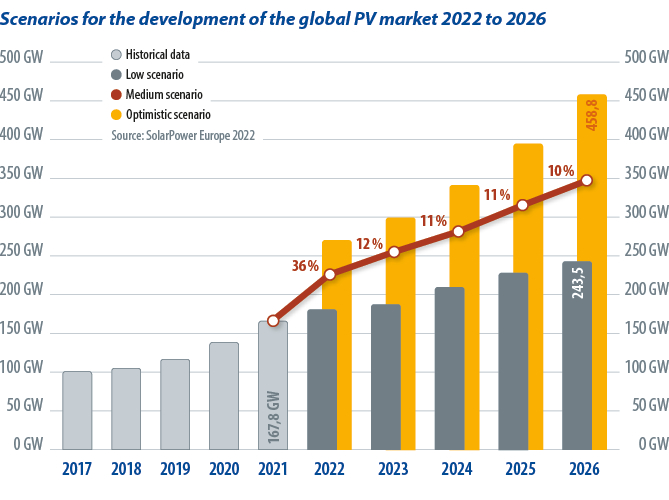

China, the United States, India, and Spain contributed 54.9 GW, 27.3 GW, 14.2 GW, and 4.8 GW of new solar capacity in 2021, respectively. The global total in the year was 167.8 GW, 21% more than was posted in 2020, when the pandemic hit. If the industry maintains the 25% average growth rate recorded over the past decade, an annual addition of 3 TW per year could be achieved within 10 years.

IEA, IRENA forecasts

SolarPower Europe expects continued strong growth and its most ambitious scenario predicts more than 300 GW of solar this year. “No single energy technology ever in history has grown as massively steeply as photovoltaics,” said Christian Breyer, professor of solar economics at Finland’s LUT University, in reference to the PV learning curve in the past 20 years.

As a result, institutions underestimate solar’s growth potential, even SolarPower Europe itself, as executive advisor Michael Schmela admitted in Berlin. Breyer pointed to frequent failures by the International Energy Agency (IEA) and the International Renewable Energy Agency (IRENA) to anticipate the meteoric rise of PV. In view of the proven dynamism of the industry and pressing need to address climate change, it is incomprehensible how IRENA can expect annual global PV installations to plateau at around 440 GW per year of new solar from 2030 to 2050.

As Silicon Valley venture capitalist-turned solar entrepreneur Bill Nussey explained in his 2022 book “Freeing Energy,” “economies of volume” are at play in the solar and semiconductor industries. In the US alone, the Inflation Reduction Act (IRA) is expected to lead to the installation of 950 million solar modules. This massive scale drives solar’s exponential growth. By comparison the global number of coal- and gas-fired power plants is tiny and this fundamental difference makes forecasting PV adoption all the more complicated.

Solar, though, needs suitable conditions to flourish and help cap the rise in average global temperature this century at 1.5 C. As LUT’s Breyer points out, it’s not just a matter of replacing fossil-fuel power plants with renewables but also of electrifying – and thus, decarbonizing – sectors including transport and industry, as part of renewables-driven power-to-X. For such a vast undertaking, 3 TW per year of solar may be too little. That’s why Breyer ventured even further in the 3,000 GW session by asking the audience whether 3 TW is “crazy, realistic, necessary, or maybe even too low.”

Breyer added, 15 to 20 years ago the world did not have 5 TW of power plant generation capacity, full stop. No-one then was mulling power-to-X and decarbonizing supply chains.

IRA as catalyst

The IRA addresses the upstream solar industry of component manufacturing as well as the downstream market of PV installations. Previously, US solar manufacturing was marked by ugly bankruptcies such as Solyndra or German business Solarworld’s Oregon subsidiary, as American companies followed in the footsteps of their European peers.

The IRA introduces a ten-year investment tax credit of 30% with “adders” to raise the credit even further, such as an extra 10% for using American components. Upstream companies can claim advanced manufacturing production credits. For example, European module maker Meyer Burger will receive $0.07 per watt for each module from its new Arizona plant. The IRA – which also opens doors for Canadian and Mexican manufacturers – creates perfect conditions for a long-term PV boom.

Similar efforts are needed in Europe and elsewhere to tackle the climate crisis and reach, or even exceed, 3 TW of annual additions.

The views and opinions expressed in this article are the author’s own, and do not necessarily reflect those held by pv magazine.

This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com.

“it is incomprehensible how IRENA can expect annual global PV installations to plateau at around 440 GW per year of new solar from 2030 to 2050.” Actually, it’s very much in line with the IEA’s absurd past predictions.

Solar is now cheaper than the 2080 figure the IEA predicted 15 years ago.

They were set up by fossil fuel interests and pay back their masters with laughable estimates of the cost and global installs of solar and wind.

I don’t think the most optimistic scenario is optimistic. The ongoing capacity expansion in China alone is already higher, and additional capacity is being created in India and the USA. And new production capacities are also being created in Europe – so far at a low level, but that can also change.

My tip for 2025:> 500 GW

I’d argue that the person who knows the most about solar power, and probably has done for the best part of 50 years, is the multi–award winning Professor Martin Green from the University Of New South Wales in Australia. His team have consistently held most world records for solar panel efficiency over the past few decades, and their PERC technology is in 75%+ of solar panels worldwide.

Even he is surprised how fast solar has grown and how cheap it has become.

He now believes that it is going to get “insanely cheap” this decade.

If he’s right, and he probably will be, 3,000 Gw annual installations may well be only 10 years away.

Personally, I’d put money on at least 1,500 Gw annually by 2030.

In round numbers it takes 30GW of PV to generate 1% of the US 4,000TWH/year electric consumption. 3,000GW of PV per year would equal the entire out of the US electric grid. That is a lot of new green power.